|

|

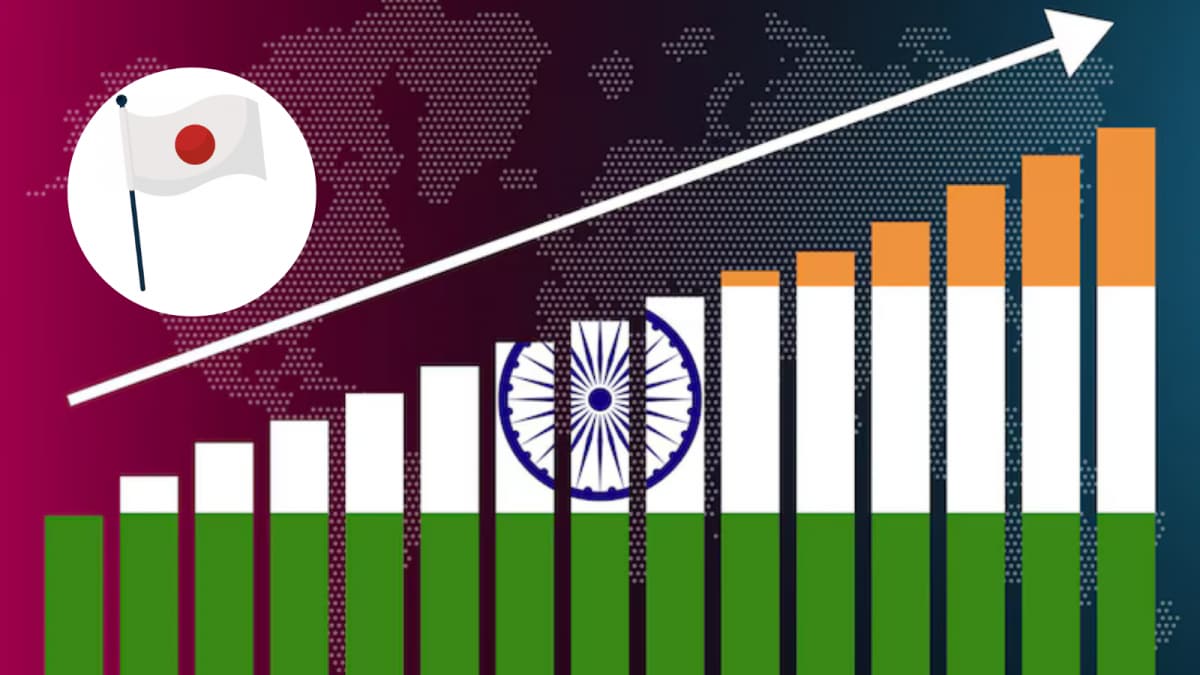

India's recent ascent to the position of the world's fourth-largest economy, surpassing Japan, marks a significant milestone in its economic trajectory. This achievement, based on data released by the International Monetary Fund (IMF) and highlighted by NITI Aayog CEO BVR Subrahmanyam, underscores India's growing economic clout on the global stage. However, a closer examination reveals a complex picture, one that encompasses both remarkable progress and persistent challenges. While India's overall GDP has reached an impressive $4.187 trillion, positioning it behind only the United States, China, and Germany, its per capita GDP remains comparatively low, highlighting the vast disparities in wealth distribution within the country. This juxtaposition of overall economic size and individual prosperity raises important questions about the nature of India's growth and its impact on the lives of its citizens. The IMF's projections for India's economic growth in the coming years are cautiously optimistic. The April 2025 edition of the World Economic Outlook forecasts a growth rate of 6.2% for 2025 and 6.3% for 2026, maintaining a solid lead over global and regional peers. These projections are underpinned by India's relatively favorable demographics and its potential to continue catching up with more advanced economies. However, the IMF also notes a downward revision in the 2025 forecast, reflecting the impact of heightened global trade tensions and growing uncertainty. This serves as a reminder that India's economic fortunes are not entirely within its own control and are susceptible to external shocks and geopolitical risks. The comparison of India's economic performance with that of other major economies provides valuable context. The United States, with a GDP of $30.51 trillion, remains the undisputed leader, followed by China at $19.23 trillion and Germany at $4.74 trillion. While India has made significant strides in closing the gap with these economic powerhouses, the sheer magnitude of the difference underscores the long road ahead. Moreover, the comparison with Japan, which India has recently overtaken, highlights the dynamic nature of the global economic landscape and the potential for shifts in relative economic power. The issue of GDP per capita is particularly critical. While India's overall GDP is impressive, its per capita ranking of 144th globally, with a value of approximately $2,850-2,900, reveals a stark reality. This figure is significantly lower than that of many smaller countries, including Luxembourg ($141,080), Switzerland ($111,716), and Ireland ($107,243). This disparity underscores the challenge of translating overall economic growth into tangible improvements in the living standards of the majority of the population. Factors contributing to India's low GDP per capita include its large population, income inequality, and the prevalence of poverty. Addressing these issues will require a concerted effort to promote inclusive growth, improve access to education and healthcare, and create opportunities for all segments of society. The IMF's analysis also highlights the potential for demographic shifts to impact India's economic growth in the long term. While India currently benefits from a relatively young population, which is expected to drive economic growth in the near term, this demographic advantage is projected to diminish over time. As the population ages, the dependency ratio will increase, and the labor force will shrink, potentially leading to a slowdown in economic growth. To mitigate this risk, India needs to invest in education and skills development to ensure that its workforce is prepared for the challenges of the future. Furthermore, it needs to create a supportive environment for innovation and entrepreneurship to foster new sources of economic growth. The global economic landscape is becoming increasingly complex and uncertain. Geopolitical tensions, trade wars, and technological disruptions are creating new challenges for all countries, including India. To navigate these challenges successfully, India needs to adopt a proactive and strategic approach to economic policy. This includes strengthening its domestic institutions, promoting regional cooperation, and engaging actively in multilateral forums. It also requires a commitment to sustainable development, ensuring that economic growth does not come at the expense of the environment or social equity. In conclusion, India's rise to the position of the world's fourth-largest economy is a significant achievement, but it is only one step in a long journey. To realize its full economic potential, India needs to address the challenges of income inequality, improve its human capital, and create a sustainable and inclusive growth model. By doing so, it can transform its economic success into tangible improvements in the lives of all its citizens and solidify its position as a global economic leader.

The implications of India's economic advancement extend beyond mere statistical rankings. It signifies a shifting global power dynamic, where emerging economies are increasingly challenging the established order. India's growing economic influence translates into greater political and strategic leverage on the international stage. Its voice carries more weight in global forums, and its partnerships with other countries become more consequential. This newfound influence brings with it both opportunities and responsibilities. India has the opportunity to shape the global agenda on issues ranging from climate change to trade and investment. It also has the responsibility to use its power wisely, promoting peace, stability, and prosperity in the region and beyond. However, India's economic rise is not without its detractors. Some observers express concerns about the social and environmental costs of rapid economic growth. They point to issues such as pollution, inequality, and displacement as evidence that India's development model is not sustainable. These concerns are valid and need to be addressed. India needs to find ways to balance economic growth with environmental protection and social justice. This requires a holistic approach to development that takes into account the needs of all stakeholders, including the poor and marginalized. One of the key challenges facing India is to create more jobs. While the economy has been growing rapidly, job creation has lagged behind. This has led to rising unemployment and underemployment, particularly among young people. To address this challenge, India needs to promote labor-intensive industries, invest in skills development, and create a more favorable environment for small businesses. It also needs to reform its labor laws to make them more flexible and responsive to the needs of the economy. Another important challenge is to improve infrastructure. India's infrastructure is still inadequate to support its growing economy. This includes roads, railways, ports, and airports. To address this challenge, India needs to increase investment in infrastructure, streamline regulatory processes, and attract private sector participation. It also needs to improve the efficiency of its existing infrastructure assets. Education is another critical area. India's education system is still not providing its citizens with the skills they need to compete in the global economy. To address this challenge, India needs to increase investment in education, improve the quality of teaching, and make education more accessible to all. It also needs to reform its curriculum to make it more relevant to the needs of the labor market. Finally, India needs to address the issue of corruption. Corruption is a major impediment to economic growth and development. It undermines trust in government, discourages investment, and diverts resources from essential services. To address this challenge, India needs to strengthen its anti-corruption laws, improve the enforcement of these laws, and promote transparency and accountability in government. India's economic success depends on its ability to overcome these challenges. By addressing these challenges effectively, India can unlock its full economic potential and create a more prosperous and equitable society for all its citizens.

The role of technology in India's economic future cannot be overstated. The country's burgeoning tech sector has already made a significant contribution to its economic growth, and its potential for further expansion is immense. From software development to e-commerce to fintech, Indian companies are at the forefront of innovation in a wide range of industries. The government has recognized the importance of technology and has launched several initiatives to promote its development, including the Digital India campaign and the Startup India initiative. These initiatives aim to create a more favorable environment for technology companies, encourage innovation, and promote digital literacy. One of the key advantages of India's tech sector is its large and talented workforce. India has a vast pool of engineers, scientists, and other skilled professionals who are capable of developing cutting-edge technologies. This workforce is also relatively inexpensive, which makes India an attractive destination for companies looking to outsource their technology development activities. However, India's tech sector also faces several challenges. One of the biggest challenges is the lack of adequate infrastructure. India's internet infrastructure is still not up to par with that of other developed countries, and this is hindering the growth of the tech sector. The government needs to invest more in internet infrastructure to ensure that all parts of the country have access to high-speed internet. Another challenge is the lack of access to funding. Many Indian startups struggle to raise the capital they need to grow their businesses. The government needs to create more opportunities for startups to access funding, such as through venture capital funds and angel investors. The regulatory environment is also a challenge. India's regulatory environment is often complex and burdensome, which makes it difficult for companies to do business. The government needs to streamline its regulations to make it easier for companies to operate in India. Despite these challenges, the future of India's tech sector looks bright. With its large and talented workforce, its growing economy, and its supportive government policies, India is well-positioned to become a global leader in technology. The tech sector can play a vital role in driving India's economic growth and creating jobs for its citizens. However, it is important to ensure that the benefits of technology are shared by all segments of society. The government needs to take steps to ensure that the digital divide does not widen and that everyone has access to the opportunities created by technology. In conclusion, India's economic journey is a complex and multifaceted one. Its rise to the position of the world's fourth-largest economy is a testament to its economic potential, but it also highlights the challenges that it faces. By addressing these challenges effectively, India can unlock its full economic potential and create a more prosperous and equitable society for all its citizens. The key to success lies in a combination of sound economic policies, strategic investments, and a commitment to inclusive growth.

Source: India Becomes 4th Largest Economy: How Far Is The No.1 Spot? A Look At Top Three GDPs